In April 2025, Zelle quietly shut down its standalone app.

No fanfare. No announcement campaign. Just a notification that if you want to use Zelle going forward, you’ll need to do it through your bank’s app or website. Over 2,200 banks and credit unions still carry it — so the network didn’t disappear. But the independent experience did.

It’s a small detail that says something large about what Zelle was always built to be: infrastructure. Reliable, fast, bank-native infrastructure. The financial plumbing of the people-to-people economy. And there’s nothing wrong with that. Zelle processed $1.2 trillion in payments in 2025, growing 20% year over year, and its “When It Counts” brand campaign — launched September 2025 — captured something genuinely true: paying the babysitter, splitting the rent, sending money to a family member far from home. Quiet acts of care, moved instantly.

But infrastructure, by definition, stays in the walls. You don’t see it. You don’t particularly feel it. You just expect it to work.

Most people, it turns out, want a little more than that from the app they open several times a week.

What everyday spending actually looks like in 2026

US consumers now make an average of eleven payments per month via mobile phone — up from four in 2018. Among adults aged 18 to 24, mobile payments account for 45% of all payments. The US mobile P2P payments market will reach $2.27 trillion in 2026, up 13.4% from the year before.

These numbers describe a generation that doesn’t think about “using a payment app” the way older demographics think about online banking. For millennials and Gen Z, paying someone digitally isn’t a feature they opted into. It’s just how money moves. The question was never whether to use a payment app. It was which one becomes the default — the one you open first, the one you suggest to the group, the one that has everyone you know already on it.

That question has a clear answer in urban America. And it’s been clear for a while.

What Zelle does well — and what it was never built to do

Zelle’s strength is directness. Bank-to-bank, instant, no fees, no app balance to manage. For transferring money to someone you already trust — a family member, a long-term roommate, a regular contractor — it’s clean and efficient. Approximately 85% of Zelle transactions relate to everyday expenses like splitting bills and paying rent, which tells you exactly who it was designed for: people making routine, known, trust-based transfers.

What it was never built for is the texture of social life. There’s no feed. No emoji. No note that says “finally 😂” after a long-overdue repayment. No way for a new contact to pay you without already knowing your bank details. No merchant QR code for the food truck at the weekend market. No way to keep a balance for casual spending. No social layer that makes the app worth opening on a day when you don’t have a specific payment to make.

Zelle is serious. Zelle is good if you regularly move money between bank accounts or send money to older family members who don’t want to see 💵💸🤑💰💲 on their transaction history. That’s a real use case. It’s just not the whole of how modern everyday spending actually works.

What Venmo was built for — and why it kept growing while others caught up

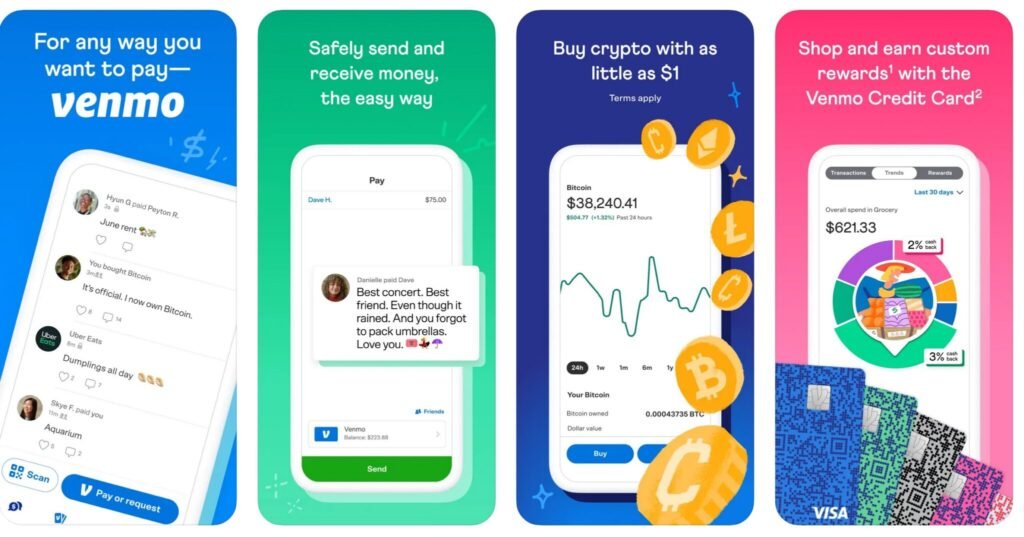

Venmo has 105 million users in 2026. Sixty-five percent of them open the app every single week. That weekly engagement number is the one that matters most — because it means Venmo isn’t a tool people reach for in a specific moment of need and then put down. It’s habitual. Embedded. The app you’re already in when the dinner bill arrives.

Venmo introduced the idea of integrating social media and P2P payments — a public, social-media-style feed of transactions where users can comment, react, and see what their network is up to financially, without seeing the actual amounts. That design decision, made in the app’s earliest years, created something no other platform in this space has fully replicated: network gravity. Everyone already on Venmo makes Venmo more useful to everyone else on it. You don’t suggest Venmo to a friend because it’s technically superior. You suggest it because you’re already on it, they’re probably already on it, and the money will land before you’ve finished the conversation.

Venmo’s payment volume reached $325 billion in 2025, with Venmo Business Profiles moving over $42 billion. Verified Merchant badges launched to help users distinguish trusted business profiles. Recurring payment and split-rent features rolled out to millions of households. Food and beverage transactions on Venmo grew 17% year-over-year, particularly in quick-service environments. The platform isn’t just for splitting dinner anymore — it’s for paying the coffee shop, settling the group Airbnb, covering the dog sitter, handling the monthly shared bills that keep a household running.

The difference between essential and habitual

Zelle is essential the way electricity is essential. You notice it when it’s missing; you never think about it when it’s working.

Venmo is habitual the way texting is habitual. You open it without deciding to. It’s already part of how you communicate, coordinate, and move through shared life with the people around you.

Both things can be true. Both platforms have a legitimate place in how America spends and shares money. But when everyday spending means groceries, weekend plans, split households, small businesses, and the thousand small financial gestures that hold a social life together — the app that does all of that, with the people you already know, in a feed that makes it feel like something rather than nothing, is the one that stays on the home screen.

For 105 million people, that app is already Venmo.

Download Venmo at venmo.com — pay, get paid, and stay connected with the people you actually spend money with.

Related Posts

Stay Informed With the Latest & Most Important News

Previous Post

Next Post

-

01Why Travel Changes Your Perspective on Life

01Why Travel Changes Your Perspective on Life -

02Benefits of Road Trips Over Other Travel

02Benefits of Road Trips Over Other Travel -

03Travel Experts Predict Top Destinations to Shape 2024 Tourism

03Travel Experts Predict Top Destinations to Shape 2024 Tourism -

04The Growing Importance of Smart Financial Planning in 2026

04The Growing Importance of Smart Financial Planning in 2026 -

05Elevate Your Everyday: Why Fabletics is the Ultimate Fusion of Fashion and Function

05Elevate Your Everyday: Why Fabletics is the Ultimate Fusion of Fashion and Function -

06Growth Mindset vs. Fixed Mindset: Understanding the Key to Personal and Professional Success

06Growth Mindset vs. Fixed Mindset: Understanding the Key to Personal and Professional Success -

07Essential Skills Every Professional Needs for Success in 2024

07Essential Skills Every Professional Needs for Success in 2024