Cash App hired Timothée Chalamet.

That’s not a joke — it’s a real campaign from July 2025, cinematic and surreal, designed to make a payments app feel like a cultural moment. It’s a well-executed piece of advertising. It’s also, if you sit with it long enough, a fairly revealing signal: when your growth strategy requires a Hollywood star to make people feel something about sending money, you’re competing for an audience that isn’t really yours yet.

Venmo has never needed a celebrity to explain what it does. Its 105 million users already get it — because most of them were there before “getting it” required any explanation at all.

Two apps. Two completely different ideas about what money should feel like.

Cash App is a financial product that markets itself as a lifestyle. It leans into aspiration — investing, Bitcoin, a cashtag that functions like a brand identity, a Timothée Chalamet campaign that reaches for Gen Z cool. The approach works in specific markets. Cash App’s adoption is strongest in the southern and midwestern United States, where it has built a genuine, loyal base of roughly 57.8 million monthly active users in 2026. That is not a small number.

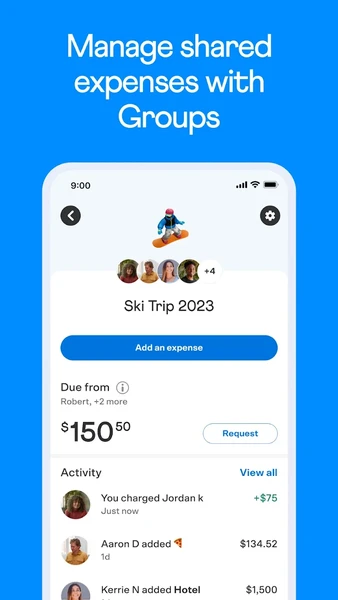

Venmo is something structurally different. It doesn’t market aspiration. It markets belonging. The social feed — transaction notes, emoji reactions, the small theatre of seeing that your friend group went to that restaurant without you — turned a utility into a cultural layer. Not a social network bolted onto a payments app, but a genuine integration of how money and social life actually work among people aged 25 to 44.

Cash App markets aspiration. Venmo markets belonging. That single distinction explains why, in high-density urban markets — California, New York, Texas — Venmo commands 37% of market share. It explains why 68% of Venmo’s user base is Gen Z or millennial. And it explains why, when someone at a dinner table says “just Venmo me,” they are not describing a transaction. They are describing a social reflex.

The numbers behind the instinct

The US mobile P2P payments market will reach $2.27 trillion in 2026, up 13.4% from 2025. Across the entire industry, 84% of US consumers have now used a peer-to-peer payment service. The shift from cash and bank transfers to app-based instant payments is no longer a demographic trend — it’s a population-level behavioural change.

Inside that market, Venmo’s position is dominant where it matters most. Over $325 billion in annual payment volume. More than 105 million users. A 73% conversion rate when merchants offer “Pay with Venmo” at checkout. Venmo Business Profiles — the QR-code and in-app merchant payment system — processed over $42 billion in 2025, with food and beverage transactions growing 17% year-over-year, particularly in quick-service environments.

These are not the numbers of a platform that followed the trend. They are the numbers of a platform that created the cultural conditions the trend grew inside.

What “instant” actually means when Venmo does it

The word “instant” appears in almost every fintech marketing campaign in 2026. It’s worth being precise about what it means in Venmo’s case — because the product delivers it in a way that goes beyond speed.

When you owe your friend money after splitting a weekend away, the Venmo notification is the receipt, the acknowledgement, and the social signal all at once. The transaction note isn’t required — but people write them anyway, because the app created space for the human layer that cash and bank transfers stripped out. “For the Airbnb 🏠” or “finally 😂” or just a string of emoji that only makes sense to the two people involved. The payment arrives in under 30 minutes to a linked bank account. But the experience it creates is immediate the moment it’s sent.

That’s what makes Venmo’s version of instant payments genuinely different from Cash App’s, from Zelle’s institutional directness, from PayPal’s transactional formality. It’s fast and it’s personal — which is why 65% of Venmo users engage with the app every single week, not once a month when a bill needs splitting.

Where Venmo is heading in 2026

The platform’s commercial expansion is deliberate and well-paced. Venmo’s B2B pilot with medium-sized retailers launched in June 2025. Recurring payment and split-rent features rolled out to millions of households. Verified Merchant badges launched to help users distinguish trusted business profiles from personal accounts. The social-commerce infrastructure that Venmo sits inside is forecast at $104 billion in the US market in 2025, and Venmo is better positioned to capture that growth than any other P2P platform — because its users are already there, already habituated, already using the app as the first answer when money needs to move.

Cash App is growing. The instant payments market is enormous enough for more than one platform to thrive inside it.

But when a payment needs to feel like something — when it’s the dinner split, the rent share, the “I’ll get you back” after a spontaneous weekend that nobody budgeted for — the app people reach for first isn’t the one with the celebrity campaign.

It’s the one that already knows how they live.

Download Venmo at venmo.com — instant payments, social by design, trusted by over 105 million users across the US.

Related Posts

Stay Informed With the Latest & Most Important News

Previous Post

Next Post

-

01Best Foods to Try in Japan

01Best Foods to Try in Japan -

0210 Smart Ways to Save Money on Your Next Hotel Stay

0210 Smart Ways to Save Money on Your Next Hotel Stay -

03Hidden Travel Gems of the World: 7 Places You’ve Probably Never Heard Of — But Should

03Hidden Travel Gems of the World: 7 Places You’ve Probably Never Heard Of — But Should -

04Global Markets Rebound as Inflation Worries Ease for Investors

04Global Markets Rebound as Inflation Worries Ease for Investors -

05Traditional Dishes Every Food Lover Should Experience

05Traditional Dishes Every Food Lover Should Experience -

06Plum Guide vs Blueground: The Rise of Premium Vacation Rentals for Modern Travelers

06Plum Guide vs Blueground: The Rise of Premium Vacation Rentals for Modern Travelers -

07Why Travel Changes Your Perspective on Life

07Why Travel Changes Your Perspective on Life