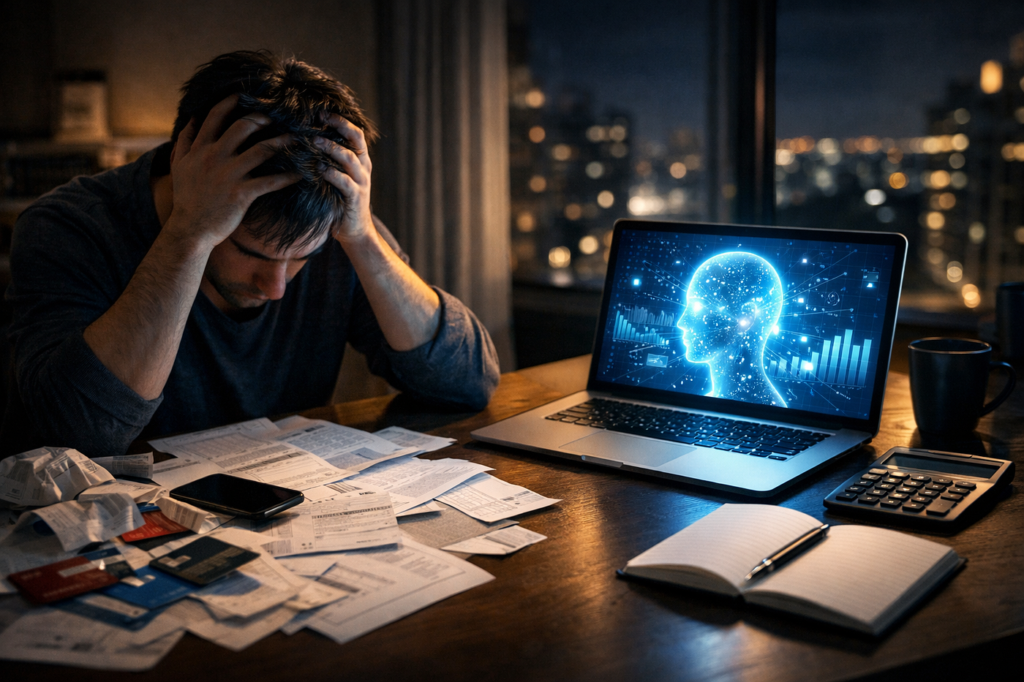

Debt has become a common financial challenge for many people in today’s fast-paced world. From credit cards and personal loans to student loans and buy-now-pay-later schemes, borrowing money has become easier than ever. While loans can help people manage important expenses, uncontrolled borrowing can quickly lead to financial stress. Many individuals find themselves overwhelmed by monthly payments and rising interest rates.

In 2026, however, there are smarter and more effective ways to deal with debt. With better financial tools, digital budgeting platforms, and improved awareness about personal finance, individuals can take control of their money and gradually move toward financial stability.

Understanding the Real Cause of Debt

Before solving a debt problem, it is important to understand how it started. Debt often builds up due to overspending, unexpected medical bills, job loss, or poor financial planning. Credit cards with high interest rates are one of the biggest contributors to rising personal debt.

Another reason people struggle with debt is the habit of making minimum payments. While minimum payments may seem manageable, they allow interest to accumulate over time, making the total amount owed much larger.

Recognizing these patterns is the first step toward creating a realistic plan to regain control of finances.

Creating a Clear Financial Plan

One of the most effective ways to tackle debt is by creating a structured financial plan. Start by listing all debts, including the total amount owed, interest rates, and minimum monthly payments. This provides a clear picture of the financial situation.

Next, prepare a monthly budget. Identify essential expenses such as rent, groceries, and utilities, and compare them with monthly income. Any remaining funds can be allocated toward paying off debt faster.

A simple budget helps individuals avoid unnecessary spending and focus on financial priorities.

Using the Debt Snowball or Avalanche Method

Financial experts often recommend two popular strategies for paying off debt: the debt snowball method and the debt avalanche method.

The snowball method involves paying off the smallest debts first while continuing minimum payments on larger ones. As each smaller debt is cleared, the freed-up money is used to tackle the next one. This approach builds motivation and encourages consistent progress.

The avalanche method focuses on paying off debts with the highest interest rates first. While it may take longer to see results, this strategy saves more money in the long run by reducing interest payments.

Choosing the right method depends on individual preferences and financial discipline.

Leveraging Technology for Financial Management

In 2026, technology has made managing finances much easier. Many mobile apps help users track expenses, monitor debt, and create personalized repayment plans. These apps provide reminders, spending insights, and visual progress reports, making it easier to stay committed to financial goals.

Digital banking tools also allow individuals to automate savings and loan payments. Automation reduces the risk of missed payments and helps maintain a consistent debt repayment schedule.

With the help of technology, people can gain better control over their financial habits.

Considering Debt Consolidation

For individuals struggling with multiple loans or credit card balances, debt consolidation can be a helpful option. Debt consolidation involves combining multiple debts into a single loan with a lower interest rate or simpler repayment structure.

This approach can reduce the stress of managing multiple payment deadlines and may lower overall interest costs. However, it is important to carefully review the terms before choosing a consolidation plan.

Financial advisors or credit counseling services can help determine whether this strategy is suitable for a particular situation.

Building Better Financial Habits

Escaping debt is not just about repayment—it also requires developing healthier financial habits. Avoiding unnecessary purchases, reducing impulsive spending, and prioritizing savings can help prevent future financial difficulties.

Creating an emergency fund is another important step. Even small monthly contributions to a savings account can provide financial security during unexpected situations.

Financial education also plays a crucial role in long-term stability. Learning about budgeting, investing, and responsible borrowing helps individuals make smarter financial decisions.

Conclusion

Debt can feel overwhelming, but it is not impossible to overcome. With the right strategies, discipline, and financial awareness, individuals can gradually regain control of their finances.

By understanding the causes of debt, creating a clear budget, choosing effective repayment methods, and using modern financial tools, people can move toward a debt-free future. The key is to start with small, consistent steps and remain committed to long-term financial health.

In 2026, the smartest way out of debt is not quick fixes or risky shortcuts—it is thoughtful planning, responsible spending, and a strong commitment to financial well-being.

Related Posts

Stay Informed With the Latest & Most Important News

Previous Post

Next Post

-

01Top Tips to Stay Motivated and Avoid Burnout While Working Remotely

01Top Tips to Stay Motivated and Avoid Burnout While Working Remotely -

02The Growing Importance of Online Payment Infrastructure in 2026

02The Growing Importance of Online Payment Infrastructure in 2026 -

03The Core Toolkit: Essential Gear Every Music Creator Should Consider in 2026

03The Core Toolkit: Essential Gear Every Music Creator Should Consider in 2026 -

04How to Travel Between European Cities: Cheapest & Fastest Options (2026 Guide)

04How to Travel Between European Cities: Cheapest & Fastest Options (2026 Guide) -

05Sleep Science Shows Why Quality Matters More Than Duration

05Sleep Science Shows Why Quality Matters More Than Duration -

06The Art of Crocheting: A Creative and Relaxing Craft

06The Art of Crocheting: A Creative and Relaxing Craft -

07Best Beach Destinations Around the World

07Best Beach Destinations Around the World